May 13, 2025

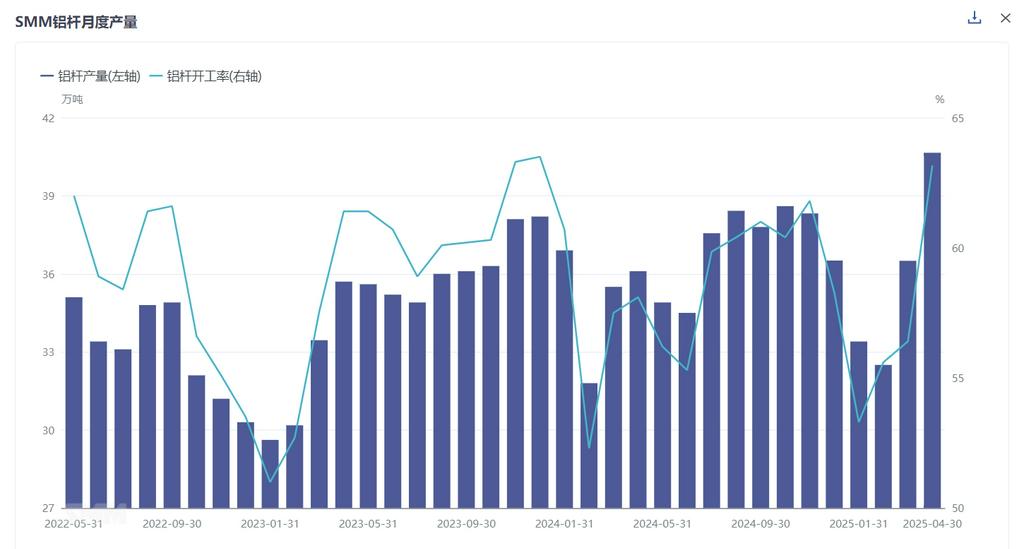

According to the latest monthly data survey by SMM, the total production of aluminum rods nationwide in April 2025 reached 406,500 mt, an increase of 41,500 mt compared to March. After adjusting for the number of days in the month, the operating rate of aluminum rod plants in April recorded 63.16%, up 6.77% MoM and 5.06% YoY. The main reason was that downstream aluminum wire and cable entered the delivery cycle, with rigid demand releasing and in-plant inventory nearly cleared. The pre-sale production schedule of orders significantly drove the recovery in operating rates. Meanwhile, the center of aluminum prices pulled back, and market buying sentiment was more optimistic YoY, promoting the recovery in aluminum rod supply-side operations.

In terms of regional operating rates, Shandong and Inner Mongolia maintained high operating rates, recording 88.9% and 80.6%, respectively, with MoM increases of 3.6% and 9.3%. Additionally, operating rates in Henan, Shanxi, Ningxia, Sichuan, and Yunnan continued to rise, with MoM increases ranging from 3% to 25%. In the market, the aluminum rod market in Q1 was affected by the accumulation of in-plant inventory. Despite rigid demand, supply was ample, and processing fees remained weak. As the market entered the resumption period and delivery cycle, in-plant inventory of aluminum rods rapidly declined, and market demand surged, leading to a shortage. Orders shifted to pre-sale status, and processing fees gained upward momentum, fluctuating at highs over the past two years.

In the market, benefiting from the tight situation in power grid construction projects, downstream aluminum wire and cable factories entered an intensive delivery phase. Under rigid market demand, aluminum rod manufacturers experienced smooth shipments, with orders mostly in pre-sale status and in-plant inventory maintained at low levels. For high-conductivity aluminum rods, current orders from the State Grid have specific requirements for high-conductivity aluminum wire, driving market consumption of high-conductivity aluminum rods. Meanwhile, the second batch of orders for ultra-high voltage transmission and transformation projects is expected to be finalized, indicating sustained consumption of such aluminum rods. For aluminum alloy rods, although the market saw a new wave of PV installations at the beginning of the year, distributed PV installations were affected by PV policies, potentially impacting the aluminum alloy wire and cable market. However, it is worth noting that centralized PV installations have had less impact, and orders in the aluminum alloy wire and cable market remain supported. Subsequent market dynamics need to be closely observed.

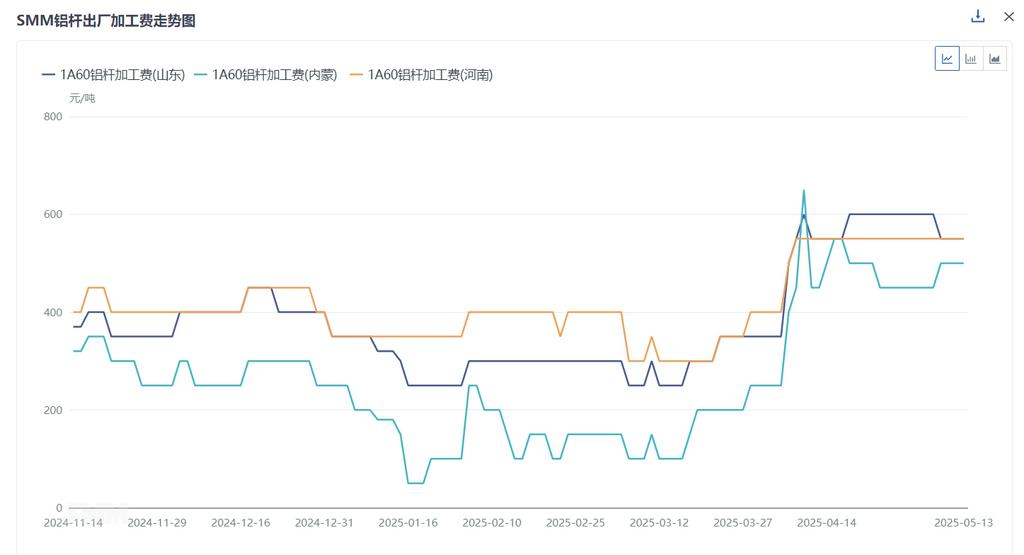

In terms of specific processing fees, the ex-factory monthly average processing fee for 1A60 in Shandong in April recorded 545 yuan/mt, up 248 yuan/mt MoM; in Henan, it recorded 526 yuan/mt, up 191 yuan/mt MoM; and in Inner Mongolia, it recorded 450 yuan/mt, up 291 yuan/mt MoM. Among the three major trading hubs, the delivered monthly average price in Hebei was 611 yuan/mt, up 269 yuan/mt; in Jiangsu, it was 711 yuan/mt, up 269 yuan/mt; and in Guangdong, it was 622 yuan/mt, up 94 yuan/mt. Processing fees across various regions generally increased this month, primarily driven by the strong demand from downstream sectors coupled with favorable buying sentiment in the market. With in-plant inventory remaining at relatively low levels from late March to early April, the market shifted towards pre-sale orders, enhancing the bargaining power of manufacturers and driving a significant increase in processing fees.

SMM forecasts that in May, the aluminum rod market may continue to experience an undersupply situation. The rigid demand from the aluminum wire and cable industry still has room to grow in terms of aluminum rod consumption. On the other hand, manufacturers' pre-scheduled production orders are expected to range from 3 to 14 days, with manufacturers operating at full capacity, indicating a certain supply gap in the market. Regarding processing fees, the significant decline in the aluminum price center in April, combined with market supply deficits, led to a surge in processing fees, reaching a near two-year historical high. It is expected that against the backdrop of bearish macro sentiment in May, there is still downside room for the aluminum price center. Coupled with sustained demand in the aluminum rod market, aluminum rod processing fees are expected to remain at highs, with limited downside room for processing fee reductions.